JHVEPhoto

Lockheed Martin: A More Dangerous World Is Bullish

Lockheed Martin Corporation (NYSE:LMT) investors have every right to feel disappointed, as even the heightened geopolitical tensions have not led to market outperformance recently.

In my last bullish LMT update in April 2024, I emphasized that the “war premium” has not been priced into the stock’s valuation. LMT is not assessed to be cheap, given its relatively tepid growth rates. I’ve determined that LMT’s thesis remains valid. The market still seems concerned about whether a slower growth cadence in US defense spending could affect buying sentiments on LMT. Therefore, the market has continued to bake in execution uncertainties into LMT’s valuation.

However, Lockheed Martin’s status as one of the leading prime defense contractors is immensely complex to surpass. LMT also has a well-diversified business across four crucial segments. Therefore, Lockheed Martin can depend on the defense spending of the US government and its allies to keep its backlog flowing.

Lockheed Martin’s Q2 earnings release will be posted on July 23. Investors will likely scrutinize LMT’s growing backlog, which reached more than $159B in Q1. In addition, the Department of Defense is expected to “resume taking deliveries of F-35 fighter jets” in the coming week. As a result, it should release a welcome $700M in payments for LMT, helping to improve its cash flow position. It should also bolster investor confidence about its execution as LMT continues the work on the software and system challenges hampering the TR-3 upgrades. However, the progressive cadence of LMT’s deliveries is already anticipated, with a “normalized delivery rate of approximately 40 jets per quarter to the US and its allies” from Q3. Therefore, I don’t expect investors to consider the updates surprising, although they are still noteworthy improvements.

The conflict in the Middle East and the war between Russia and Ukraine are expected to persist. Although Israel and Hamas have reportedly been working on a deal through the US and other mediators, nothing firm is in place. As a result, it should continue supporting LMT’s businesses, given their criticality to the West’s overall defense strategy.

Israel has a deal with LMT to receive new F-35 jets starting in 2028. These were part of a recent $3B agreement, with a delivery rate of 5 jets per year. Germany could also ramp up its defense spending, “focusing on significant military expansions and modernization.” As a result, LMT could receive additional F-35 orders from Germany as part of the country’s “defense expansion strategy.” In addition, the recent $2.3B arms package announced by the Biden Administration for Ukraine also includes “long-term contracts.” Therefore, it underscores the ongoing opportunities for LMT, as “$2.1B will be allocated” to LMT and RTX (RTX) under long-term funding initiatives.

There are increased concerns regarding the improved ability of Russia to deploy electronic warfare against some of LMT’s defense products. Lockheed Martin also acknowledged that it may have affected the performance of their precision capabilities. However, Lockheed Martin assures investors that the company “continually adjusts systems to address evolving challenges.”

As a result, LMT isn’t standing still and is confident that Lockheed Martin’s “proactive approach” in responding to new threats and countermeasures should prove effective. I also assess that LMT’s integrated defense portfolio’s deep complexities and highly classified nature place it in a commanding position. Therefore, it should help anchor Lockheed Martin’s leadership advantage as the West upgrades its defense strategy to respond to the threat from Russia.

The US and its NATO allies are also said to have pledged to “ramp up weapons production to support Ukraine in the face of ongoing Russian aggression.” As a result, I assess it should help bolster the current low-growth US defense spending from 2025, as NATO recognizes the threat against an increasingly aggressive Russia. Furthermore, Russia and China have forged closer ties in response to the “alienation” from the West. As a result, the higher perceived threat from these two major world powers should intensify NATO’s approach to strengthen its defense partnership and upgrade its military capabilities. Therefore, LMT is expected to continue thriving under such dangerous times as it expands its revenue exposure to international markets.

Lockheed Martin: Needs To Execute Against Its Growing Backlog

{kind=link}

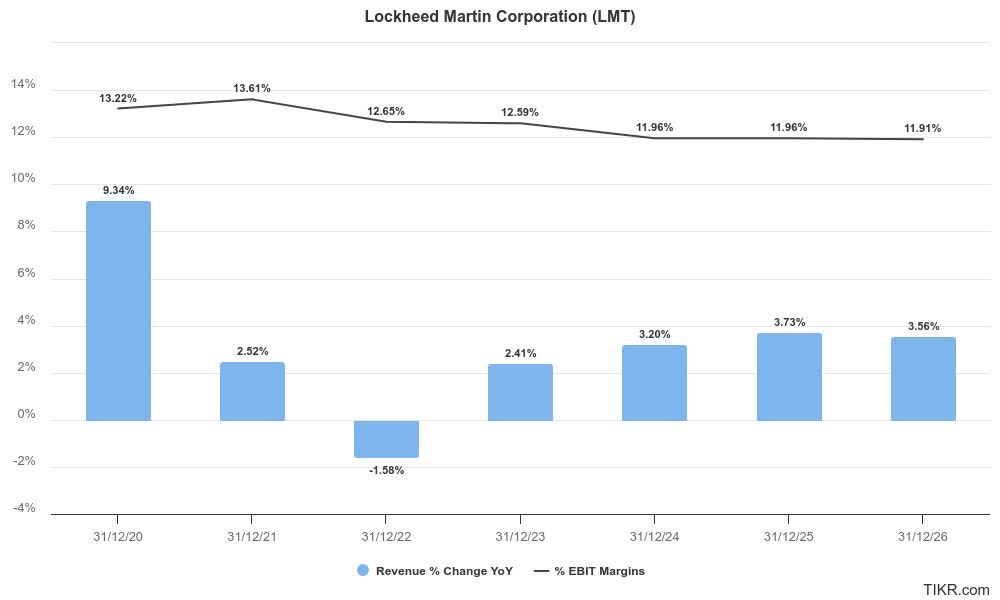

Notwithstanding my optimism, it’s incumbent on Lockheed Martin to execute well and justify its ability to benefit from an increasingly dangerous world. Lockheed Martin underscores its confidence in converting its growing backlog into potentially “mid-single digit growth rates over the next five years.”

Upgraded Wall Street estimates on LMT suggest analysts are still cautious about management’s optimism. Lockheed Martin also cautioned about the need to reflect higher execution risks attributed to the “supply chain challenges affecting operational cadence and moderating growth projections.” As a result, investors must continue monitoring LMT’s ability to lift its “operational efficiencies and program ramp-ups” to justify a faster revenue growth inflection.

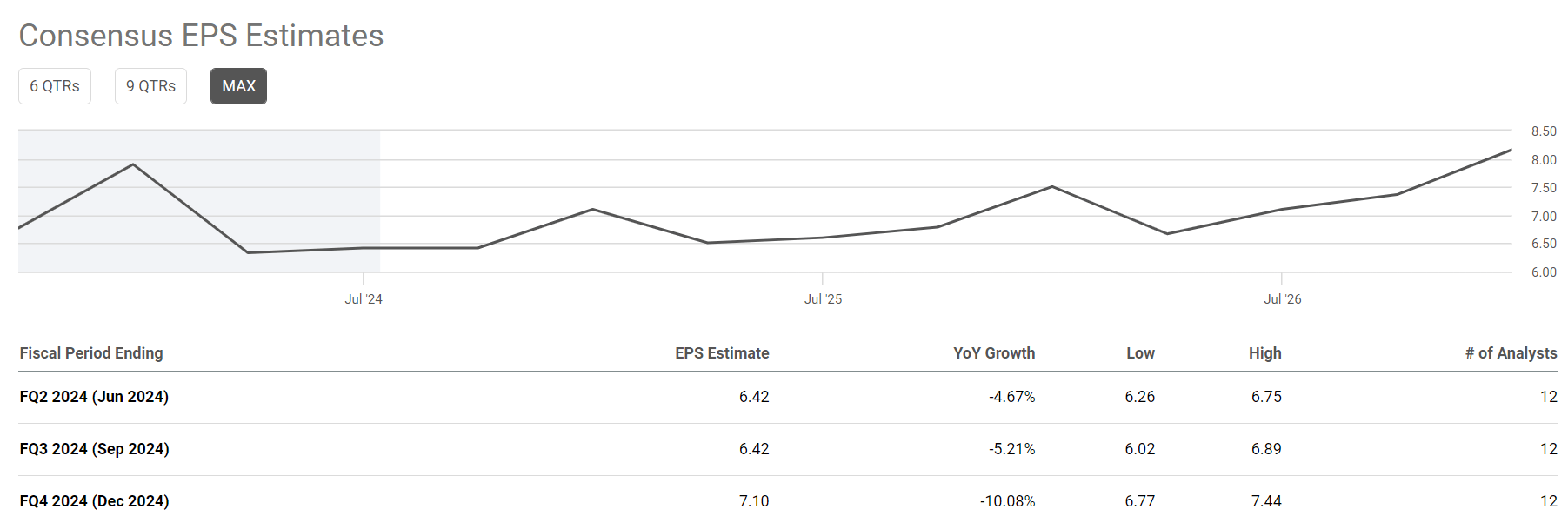

LMT EPS estimates (Seeking Alpha)

{kind=link}

Notwithstanding Wall Street’s optimism, LMT is estimated to undergo an earnings normalization phase through FQ4. As a result, it could impact buying sentiments, unless LMT could execute better against its backlog, improving deliveries.

Therefore, investors must continue to monitor LMT’s progress closely, given the opportunity for an accelerated growth inflection in LMT’s earnings estimates.

LMT: Valuation Isn’t Expensive

LMT Quant Grades (Seeking Alpha)

LMT’s “C” valuation grade supports my thesis that LMT isn’t expensive. However, caution is still justified, given its relatively weak “D-” growth grade compared to LMT’s sector peers.

However, Lockheed Martin’s high-quality business model and stable profitability should continue to maintain investor confidence. Even as it navigates challenges in converting its growing backlog, it should provide revenue visibility as LMT executes its deliveries. As a result, I don’t expect LMT to suffer a steep selloff, suggesting dip-buying sentiments should remain robust.

Is LMT Stock A Buy, Sell, Or Hold?

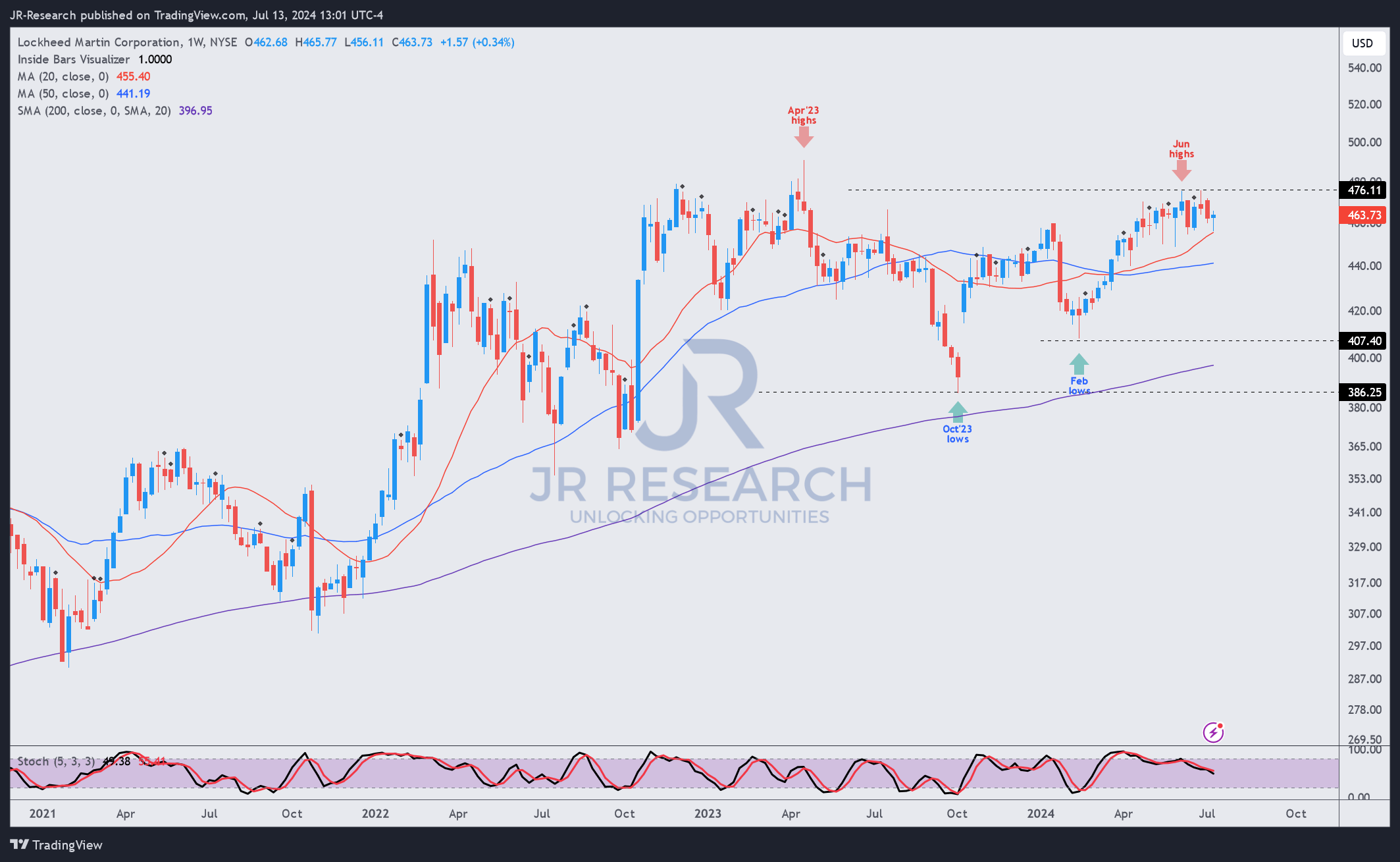

LMT price chart (weekly, medium-term, adjusted for dividends) (TradingView)

{kind=link}

Aside from LMT’s reasonable valuation, LMT’s forward dividend yield of 2.7% should also underpin its bullish thesis. However, it’s not expected to be a key valuation driver, as investors should remain focused on LMT’s execution.

LMT’s uptrend bias hasn’t been materially impacted, corroborating its uptrend continuation thesis. However, although there are no sell signals, LMT has faced notable challenges in overcoming the $475 resistance level.

Hence, I’ve assessed that LMT seems to be consolidating well, suggesting a breakout appears imminent. LMT’s dip-buyers have also been observed to underpin steep pullbacks in October 2023 and February 2024, bolstering investor confidence. Therefore, I assess LMT’s reasonable valuation is aligned with supportive geopolitical tailwinds. Coupled with LMT’s solid company fundamentals, it should support my bullish proposition.

Notwithstanding my optimism, investors must continue monitoring the progress in the F-35 upgrades. LMT’s F-35 programs have faced challenges, particularly in its TR-3 upgrades. A slower-than-anticipated resolution of the software and platform issues could hamper LMT’s ability to meet its deliveries performance.

Also, LMT mainly relies on the US government for its revenue base. Accordingly, the US government accounted for almost 74% of its Q1 revenue, reflecting significant concentration risks. As a result, unanticipated revisions to US defense spending could markedly impact LMT’s revenue visibility moving ahead, affecting buying sentiments.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!